There is no simple answer. Theories diverge. Some analysts believe that highly profitable stocks should trade on low valuation multiples based on the idea that excess profit is unsustainable. For cyclicals, a low multiple would therefore imply the high end of the cycle has been reached. This approach is known as rational anticipation. On the other hand, others believe that excess profit reflects an undeniable competitive advantage which is worth a premium and justifies high valuation multiples. This is known as the extrapolative anticipation approach.

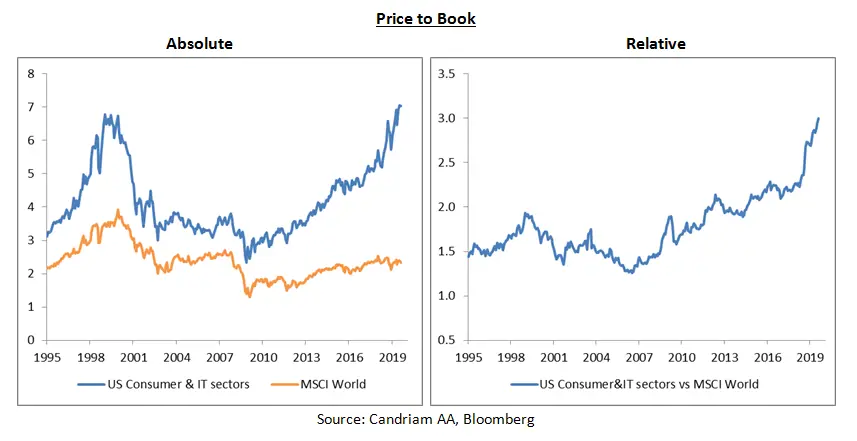

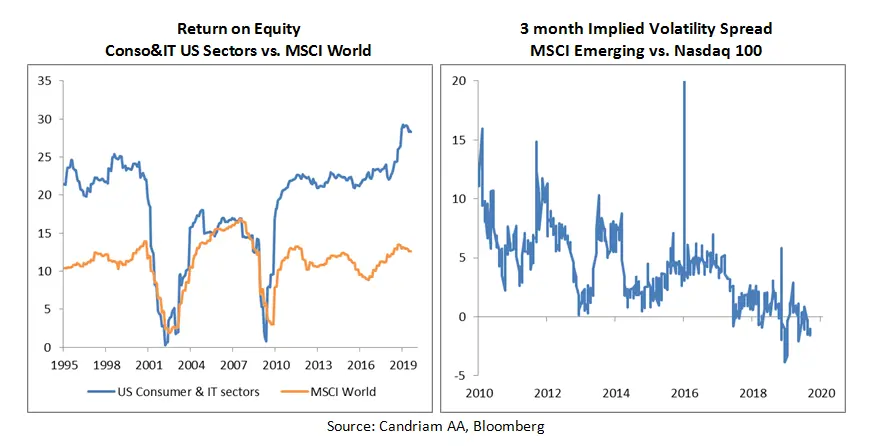

An analysis of profitability within the 3 sectors referred to above effectively reveals a relatively wide surplus (below left chart). The sustainability of this surplus is therefore a key question as it appears to be the trigger for valuation premiums.

It should be noted however that valuation premiums can deflate without there necessarily being a profitability shock. This factor has been demonstrated in the past. The chart below shows how valuations spiked previously in January 1999, whereas profits did not fall until two years later.

Lastly, expensive stocks are supposed to incur lower investment risk due to their intrinsic quality. In the event of economic and/or financial stress, they would be perceived as safe havens. However, the status of less volatile defensive stocks is being undermined, which could serve as a warning. The right hand chart above compares implied volatility in the Nasdaq 100 with the MSCI emerging markets index. The Nasdaq 100 is the emblem of innovative growth stocks, whereas the MSCI emerging index is considered to be a riskier high beta asset, although its risk profile has changed over the past few years with the increasing weight of tech stocks, notably from China.

Implied volatility in the MSCI emerging markets index has been historically higher, which corresponds with its status as a risky index, despite its relatively stronger growth outlook. 2019 bucked this established trend however. Today, in the options market, the Nasdaq100 is perceived as incurring the highest risk. It is difficult to identify the fundamental changes which have occurred in terms of its relative perception over the past year. This change may therefore represent an initial sign of investors questioning the sustainability of profits among the most expensive stocks.

Finally, valuation multiples can be seen as confidence indicators. If doubt creeps in and confidence is undermined, for the right or wrong reasons, a mean reversion process may then be triggered.